Since shortly after 1859, oil has been subject to attempts to control its price, or should I say the price of its refined product, be that kerosene for lighting or, later, gasoline for autos. The first one to try was John D Rockefeller with his development of the Standard Oil Trust in the 1860s and beyond. OPEC, or the Organization of Petroleum Exporting Countries, is the latest attempt, dating back to the 1960s, and is based around the export of oil by the global low-cost producers, in particular Saudi Arabia. In effect, the Saudis, as price leaders, try to keep the price stable by varying their own production and pricing so as to discourage its erstwhile partners from both overproduction and short-term greed. Generally, when prices are high, their cheating is rampant and when prices are low, their cheating is rampant.

Well, here we go again. The price of oil is going down gradually post-Covid, dragging with it all kinds of nasties and pleasantries. This was eminently predictable: only the timing was mysterious. Let’s look at some of them.

First we have the prophets of ‘peak oil’, who keep predicting the imminent decline of supply and the rocketing upwards of price as an oil-dependent world fights over who will drive and who will walk. The reality is that the real, or non-inflationary, price of every natural resource commodity you can think of, including oil, has, on average, declined over the past 200 years and seems to keep declining. Yes, there are price bubbles, but they pop sooner or later. If the price gets too high, then it pays someone to go out and find the next most expensive ore bed or oil pocket and exploit it. The price bubble lasts about as long as it takes for a lot of new supply to come on stream. The bubble pops, the price goes down, and the marginal suppliers shut down until needed. Then the cycle repeats itself.

If you want to see this in action, go to the following and set it on ‘imported oil’ and look at real prices since the 1970s: http://www.eia.gov/forecasts/steo/realprices/

If you want to go back further for real prices, say, to the 1860s, try this site: http://chartsbin.com/view/oau

Today, oil prices are also starting to be affected by the oversupply of conventionally produced electricity due to solar and wind power price declines. A combination of government-mandated or subsidized shifts from coal and oil-powered generation, plus greater price efficiencies in alternative power sources are cutting into the market for oil. So are auto efficiencies, such as mandated greater average mileage per unit of fuel, or the gasoline-electric hybrids in cars, having their effect on oil. Granted, these do not constitute a big cut, but every time world oil prices shift upwards, these alternatives take a bigger nibble out of the oil market. It doesn’t take much of a loss in market share to affect the producers.

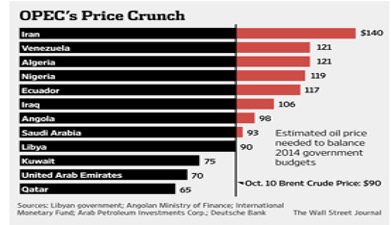

One of the big nasties from any oil price drop has to do with places that derive most or all their public revenues from the sale of oil. The budgets of countries like Venezuela or Iran are almost completely dependent on oil sales for their government revenues. Further, the price bubble since 2009 has left them dependent on a high price to cover rising public expenditures used to buy off political dissent. There are many estimates of what different oil countries need to break even, and here is one from a Wall Street Journal article. When the article you are reading was written, the price was $80 and expected to fall more.

Note that Saudi Arabia, perhaps the world’s lowest cost-of-production country, has to get a high price to keep its budget in balance. Of course, it can tap into savings or borrow, but consider the problems faced by higher-cost producers like Venezuela, racked by internal dissent, or Iran or Russia, subject to all sorts of financial restrictions. For them, this is not good news.

When the price drops, these countries can do a number of things: they can borrow, if their credit is good, or they can cut expenditures, though many of these countries subsidize consumer energy expenditures, cutting thus being a sure formula for unrest, or they can produce more, cheat on OPEC and keep the game going in the short run. Of course, this last option can’t work forever and it will just drive the price of oil lower overall. Generally, countries with domestic unrest will either concentrate on keeping the lid on through repression or they will go off on some international adventure to mask the problem with some nationalist fervor. Take your choice. Take today’s Iran and Russia…

Another set of losers are the environmentally-friendly alternatives, since they are all ‘high-cost producers’ and their competitiveness becomes squeezed with low oil prices. The instability in oil prices over the past 30 years has meant that companies providing alternative energy always face the difficulty in acquiring long-term financing for research and for product sales precisely because the time horizons between price peaks or slumps is too short for potential investors’ comfort.

In countries where there is little or no oil production, some pleasantries do happen. The price of fuel goes down and this acts as a pay raise for their people, rich and poor. A lower oil price has effects throughout the consumer economy as producers and final consumers both save money. This can have differential effects on a national economy like Canada’s. Alberta’s revenues will drop, while Ontario’s economy will get a boost. Exploration and development may slow in the West and offshore. Further, the Canadian dollar drops as the value of Canada’s oil exports drop, helping other, perhaps manufacturing-based, exports to do better. The drop in the dollar acts as a kind of a relative pay cut for workers and a price rise for anyone who consumes imports. Cheap domestic labour coupled with higher prices for imported consumer goods can do wonders for politicians: Canadian Prime Minister Chretien and Finance Minister Paul Martin revolutionized the Canadian fiscal regime 2 decades ago while the media stayed mesmerized by an export boom.

Likewise, Texas’ economy may be hit while New York’s may get a boost. Or, not quite. Oil has constituted a large proportion of American imports for a long time, but the recent price bubble has encouraged the production of oil from American shale on a massive scale, leading to fewer imports. America may, for the first time in about a century, become a non-importer or even a net exporter of oil. The result will be a continual boost in the value of the American dollar. Non-oil producing States may benefit from cheaper energy, but that may be offset by the stronger dollar. China and other overseas manufacturers may find this a blessing.

As far as I am concerned, the probability is that an oil price around $80 per barrel will last for a number of years. This will change the nature of international politics. We will speculate on this in Part 3.